Initial Funding:

- 1,000 shares

- $10/share

- Total value = $10,000

GRAT Term: 2 years

7520 Hurdle Rate: 5%

Annuity Structure: Zeroed‑out GRAT (remainder ≈ $0 for gift‑tax purposes)

Payment Method: In‑kind stock only

No stock sales inside GRAT

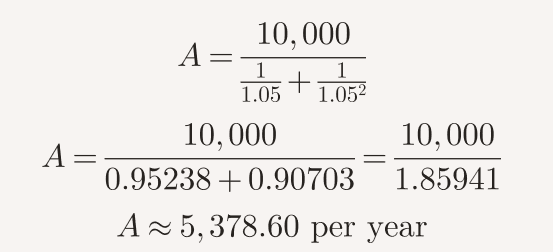

Calculate Required Annuity Payments Back to Grantor

A 2‑year zeroed‑out GRAT with a 5% hurdle rate requires annuity payments that return the present value of $10,000.

The math:

So the GRAT must pay you:

Year 2 annuity: $5,378.60

Year 1 annuity: $5,378.60

Assume Stock Appreciates

Let’s assume:

End of Year 2 price = $30/share

End of Year 1 price = $20/share

GRAT Pays Annuities in Shares

Year 1 Payment:

Stock price = $20/share

GRAT owes you = $5,378.60

Annuity at end of year 1 = 5378.60/20 ~= 269 shares.

After Year 1:

- Shares contributed: 1,000

- Shares returned to you: 269

- Shares remaining in GRAT: 731

Year 2 Payment:

Stock price = $30/share

GRAT owes you = $5,378.60

5378.60 / 30 ~= 179 shares

After Year 2:

- Shares remaining before payment: 731

- Shares returned to you: 179

- Shares left in GRAT: 552 shares

Value of Remainder to Beneficiary

Beneficiary receives all remainder value, in stock or cash, tax-free.

What happens to voting right of the stock?

Grantor can be the voting trustee of GRAT and beneficiary trust, but grantor cannot benefit financially from beneficiary trust.