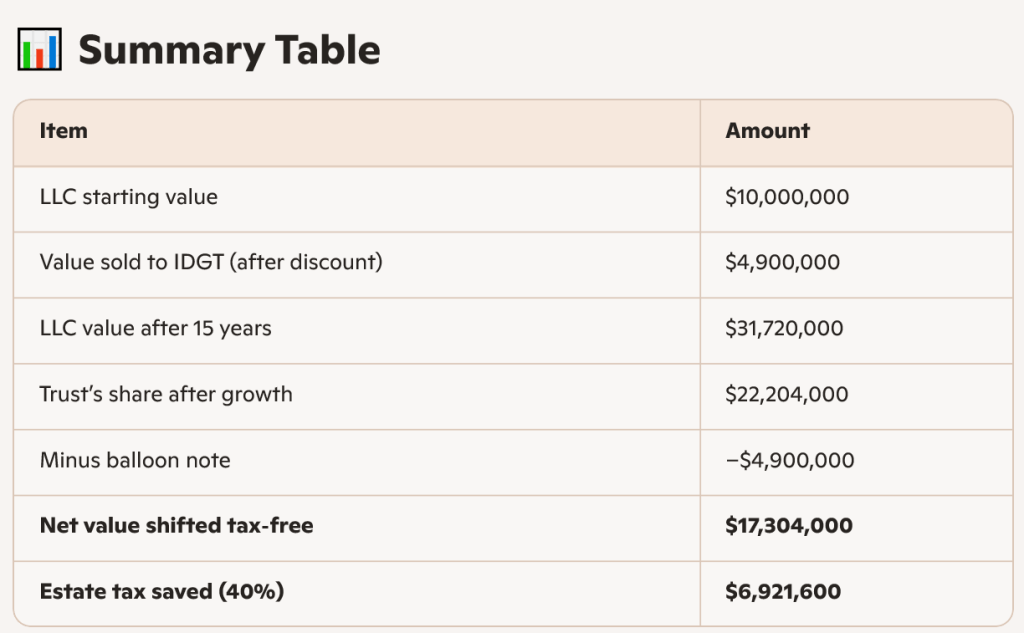

🧩 Step 1 — Start with a $10M LLC

Assume:

- Fair market value: $10,000,000

- You recapitalize into 30% voting / 70% non‑voting

- You sell the 70% non‑voting to the IDGT

🧩 Step 2 — Apply valuation discounts

Typical combined discount (DLOC + DLOM): 30%

So the 70% interest is appraised at:

10,000,000 * 70% =7,000,000

Apply 30% discount:

7,000,000 * (1-30% )=4,900,000

✔ The trust buys $7M of value for $4.9M

This discount is a legal, IRS‑recognized estate‑planning benefit.

🧩 Step 3 — The IDGT gives you a promissory note

Assume:

- AFR (long‑term) = 4%

- 15‑year interest‑only note with balloon payment

Annual interest:

4,900,000 * 4% =196,000

The trust pays you $196k/year.

🧩 Step 4 — Assume the LLC grows at 8% per year

This is conservative for a private business or real estate LLC.

After 15 years:

10,000,000 * (1.08)^15 ~= 31,720,000

So the LLC grows from $10M → $31.7M.

Your retained 30% grows to:

31,720,000 * 30% =9,516,000

The trust’s 70% grows to:

31,720,000* 70% =22,204,000

🧩 Step 5 — Trust pays off the balloon note

At the end of 15 years, the trust owes you:

- Principal: $4.9M

- You’ve already received 15 years of interest: $2.94M

The trust pays the $4.9M balloon using:

- LLC distributions

- refinancing

- or partial sale of assets

After paying the note, the trust still owns:

22,204,000-4,900,000=17,304,000

✔ $17.3M is now outside your estate.

🧩 Step 6 — Estate tax savings

Estate tax rate: 40%

Savings:

17,304,000 * 40% =6,921,600

⭐ You save about $6.9 million in estate tax.